The wine industry in 2022

On the positive side, price rises mean the total overall value of international trade in wine has reached the highest value ever recorded, increasing from €34.4bn in 2021 to €37.6bn in 2022. However, wine exports actually declined globally by 5% to 107mhl, compared to the historic high of 112.3mhl recorded in 2021. So, what’s going on?

Let’s look at the latest wine industry facts and figures in more detail.

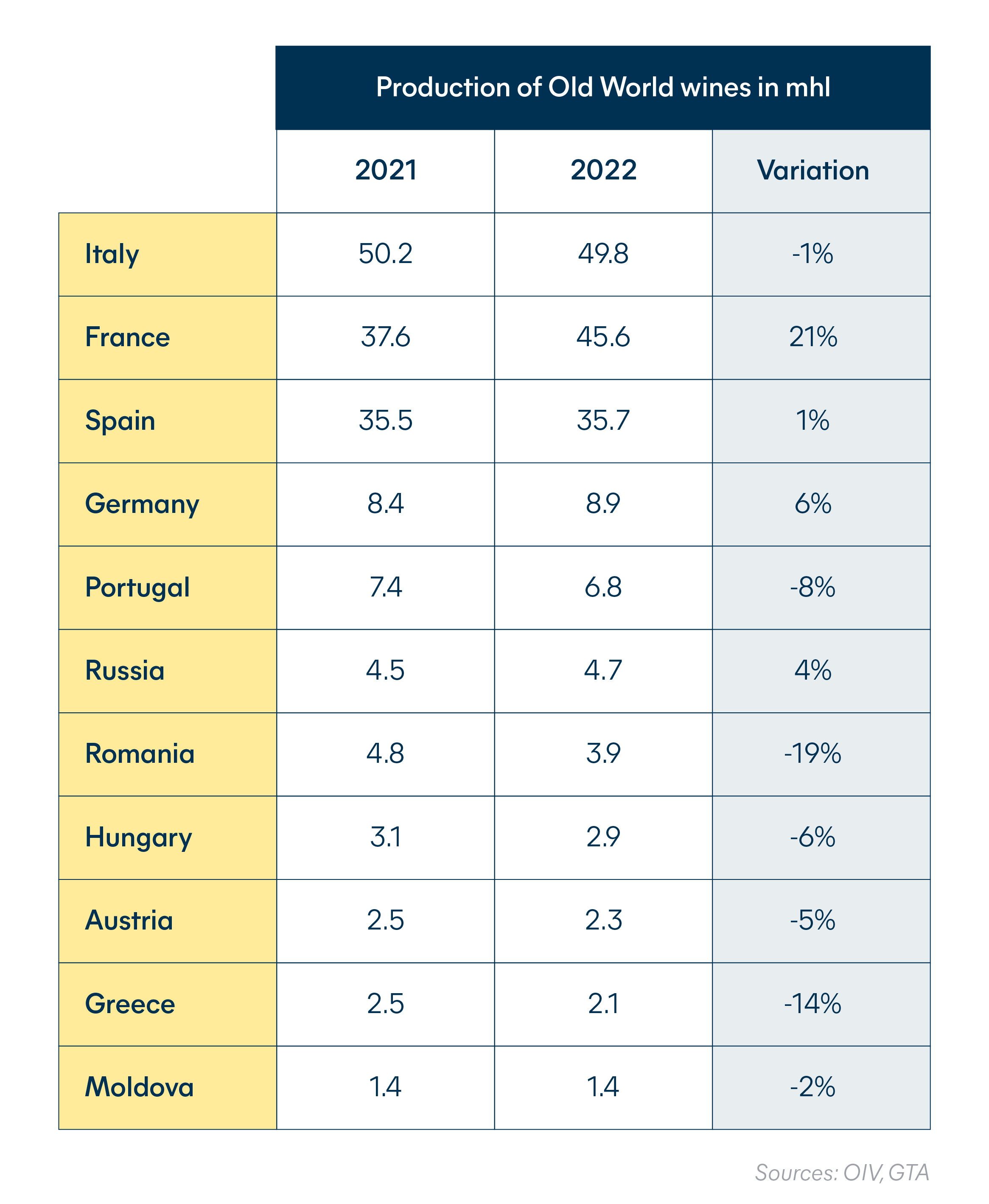

Production in Old World wine countries

The Old World EU countries of Spain, France, and Italy continue to dominate over the wine industry and still account for 51% of the world's total wine production by themselves.

For France, the last year saw a significant 21% rise in volume which also represents a 7% gain on the five-year average. Production in Spain rose just 1%, a figure that puts it 5% below its five-year average. Meanwhile, Italy saw a 1% fall in annual wine production, but a 2% increase compared to its five-year average.

Production in Germany was 6% higher but the other main Old World wine countries all saw production levels drop and in Greece, volume was at one of the lowest levels in decades.

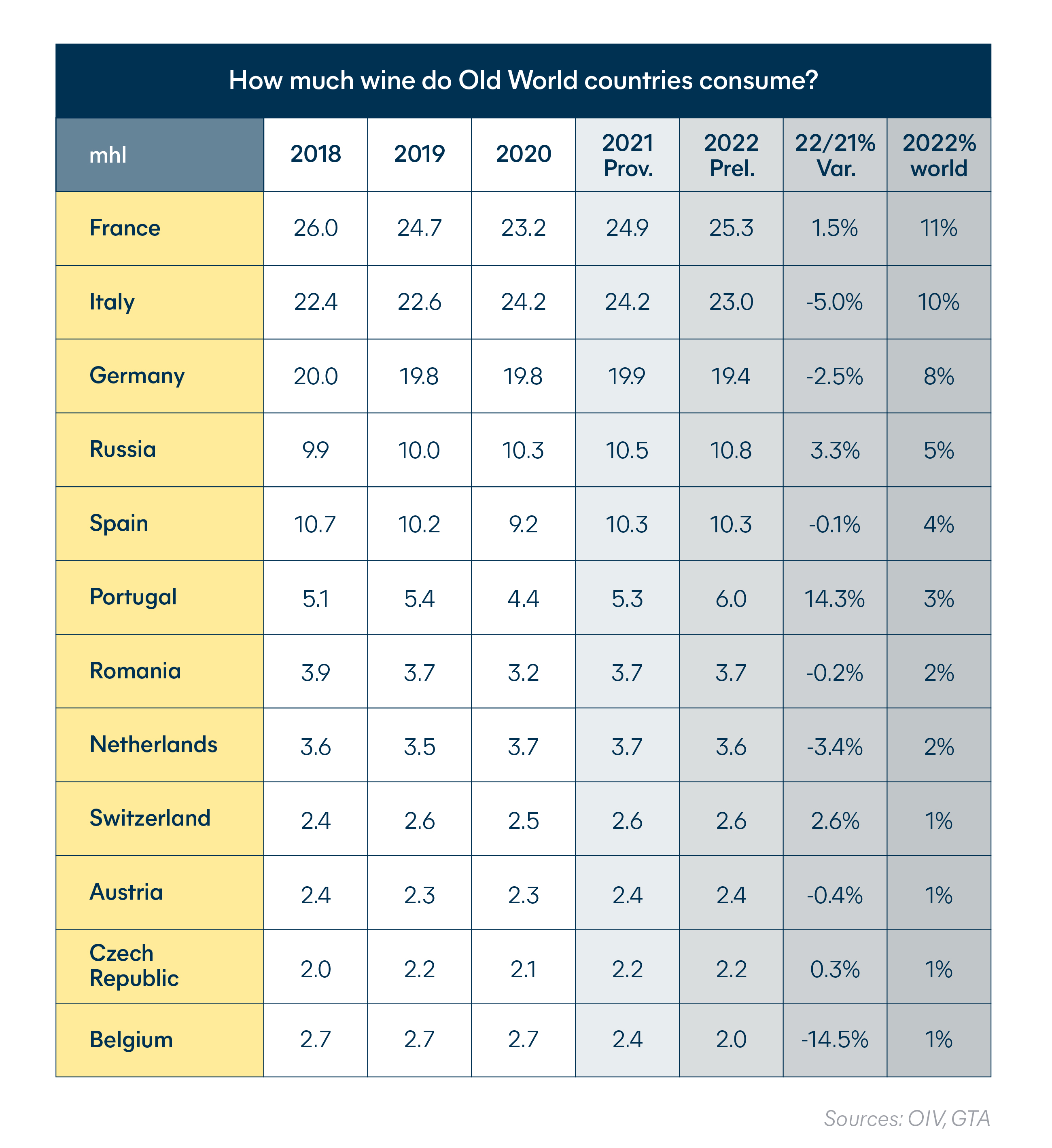

How much wine do Old World countries consume?

France takes the lead in total Old World consumption. The estimated 25.3mhl of wine bought by the French also ranked them second globally behind the US.

Demand for Old World wine over the last 5 years

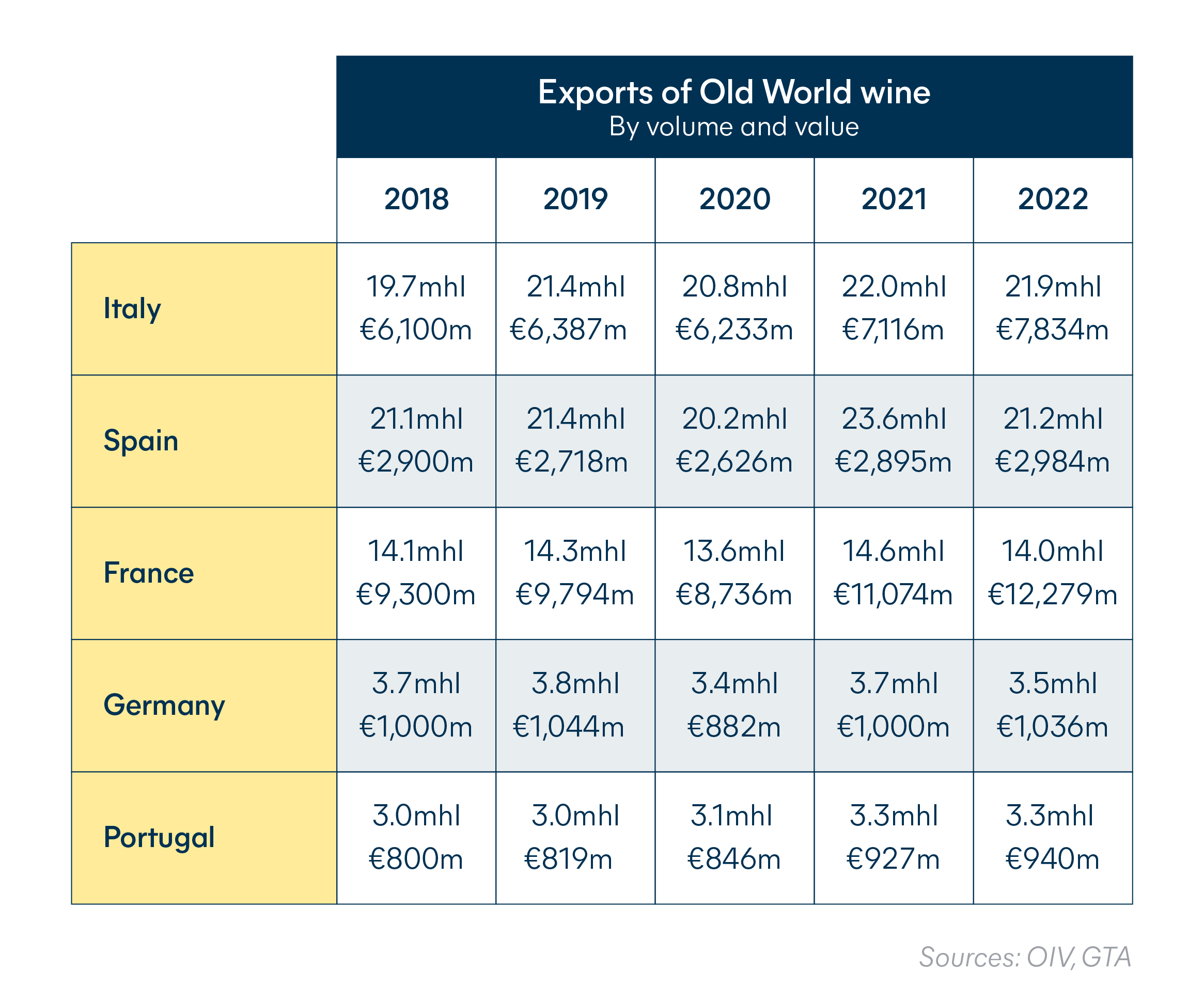

Although exports from the top three wine countries have all fallen compared to 2021, Italy, Spain, and France still accounted for 53% of world wine exports and 61% of value, exporting a total of 57mhl in 2022.

Italy came first, with exports dropping just 0.6%. Despite this, 2022 was still the country’s second-best export year in half a decade and value rose by €717m. France’s volume fell 5%, but with exports generating €12.3bn, it remains top in value, claiming almost one-third of all global export value. Spain suffered a decrease in volume of 10% and a modest 3.1% rise in value.

How much do Old World countries import?

Germany is the second largest wine importer in the world after the US. But in 2022, Germans imported 9.3% less wine by volume and value dropped to €2.7bn, a loss of 4% compared to 2021.

Globally, the UK comes in third with a volume of 13mhl imported in 2022, but imported 2% less in 2022. However, value rose sharply in all categories to reach €4.8bn. Sparkling wine in particular saw a 41% increase over 2021.

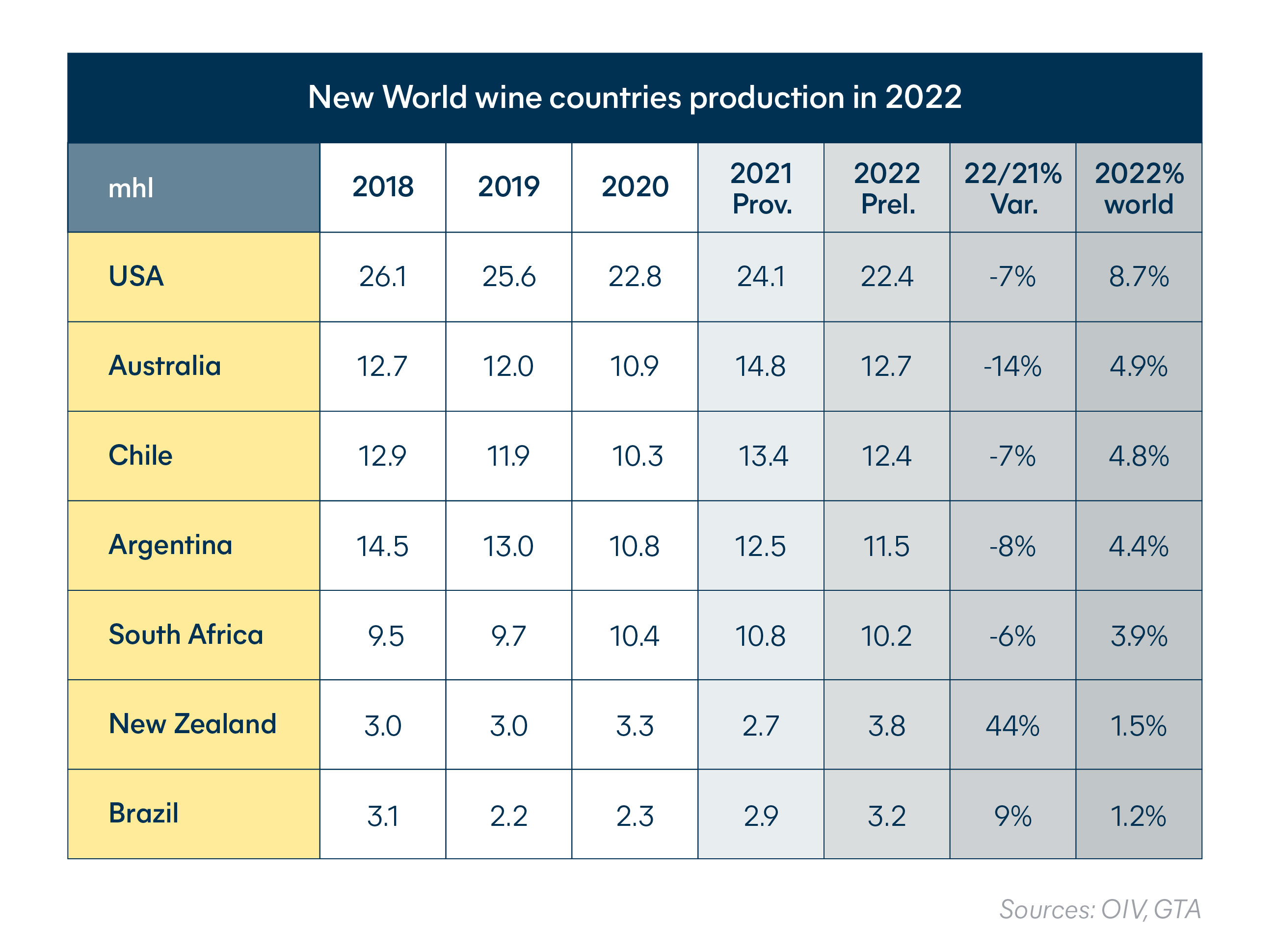

New World wine countries production in 2022

Top producer the US saw output decline 7% below the previous year and 9% below its five-year average. This trend was repeated in the two leading South American producers. Chile saw a decline of 7% and Argentina 8%. However, in Brazil, production was up 9% and 14% above the five‐year average.

In Oceania, in Australia output dropped 14%, but New Zealand enjoyed a hefty 44% surge achieving a record-high of 3.8mhl.

Exports from New World wine countries in 2022

The main New World wine countries all saw a fall in export volume except Australia, where volume rose 1.3%, and Canada where exports remained steady. However, the general rise in the price of bottled wine means most of these losses were offset somewhat by an increase in value.

Argentina saw the steepest drop with a 21% decrease in relative volume compared, but enjoyed a 7.4% rise in value. While wine exports from the US were down 14.7%, value increased by 11.8% to reach €1.4bn.

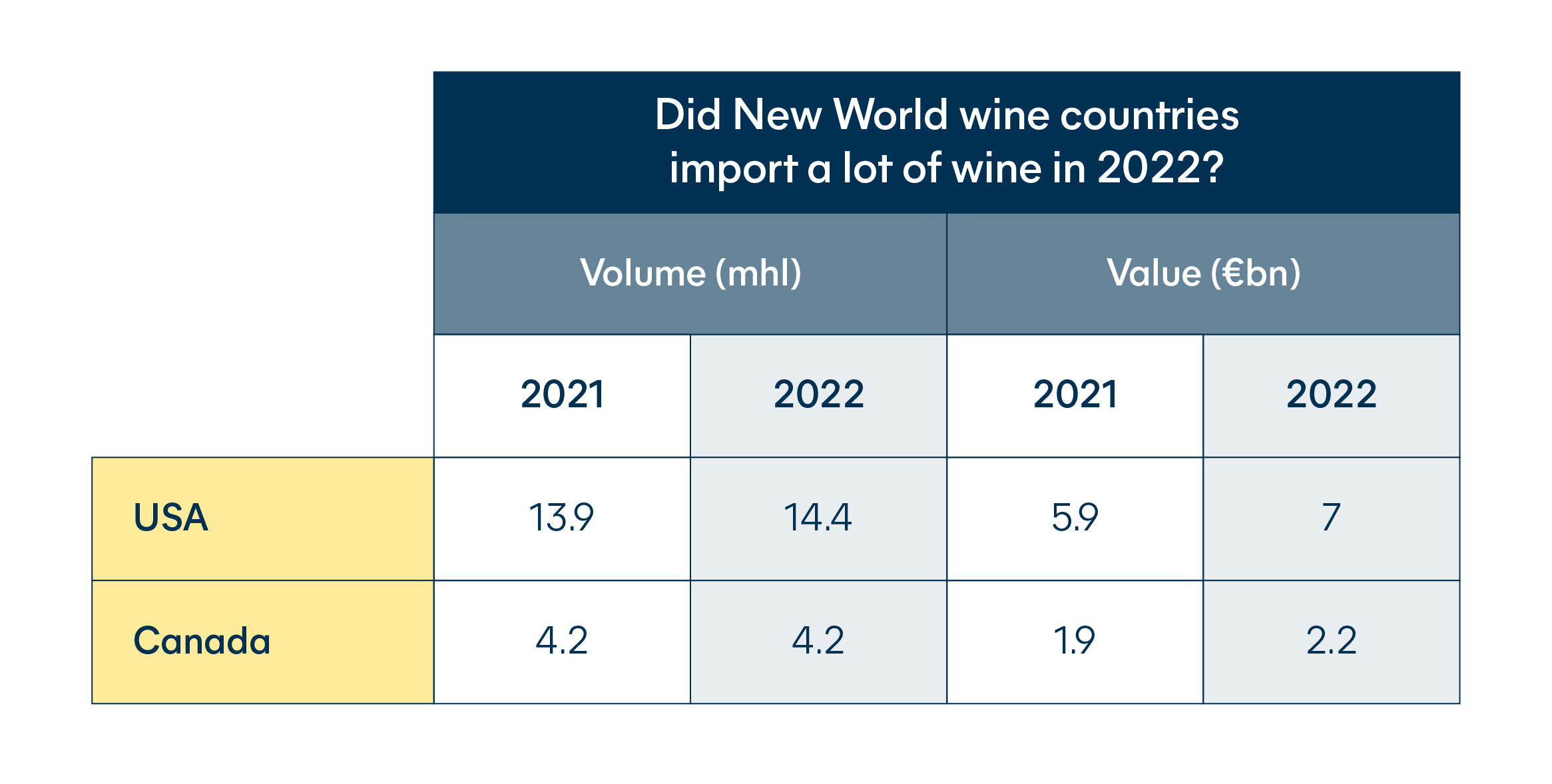

Did New World wine countries import a lot of wine in 2022?

Only the US and Canada make the top 10 when it comes to global wine imports. The US imported 14.4mhl, 3% more than 2021. Value totaled €7bn, an increase of 17%. This means the US remains the world’s largest wine importer by volume and by value.

While the 4.2mhl imported by Canada in 2022 equaled the volume for 2021 the €2.2bn spent represented a 14% rise in value.

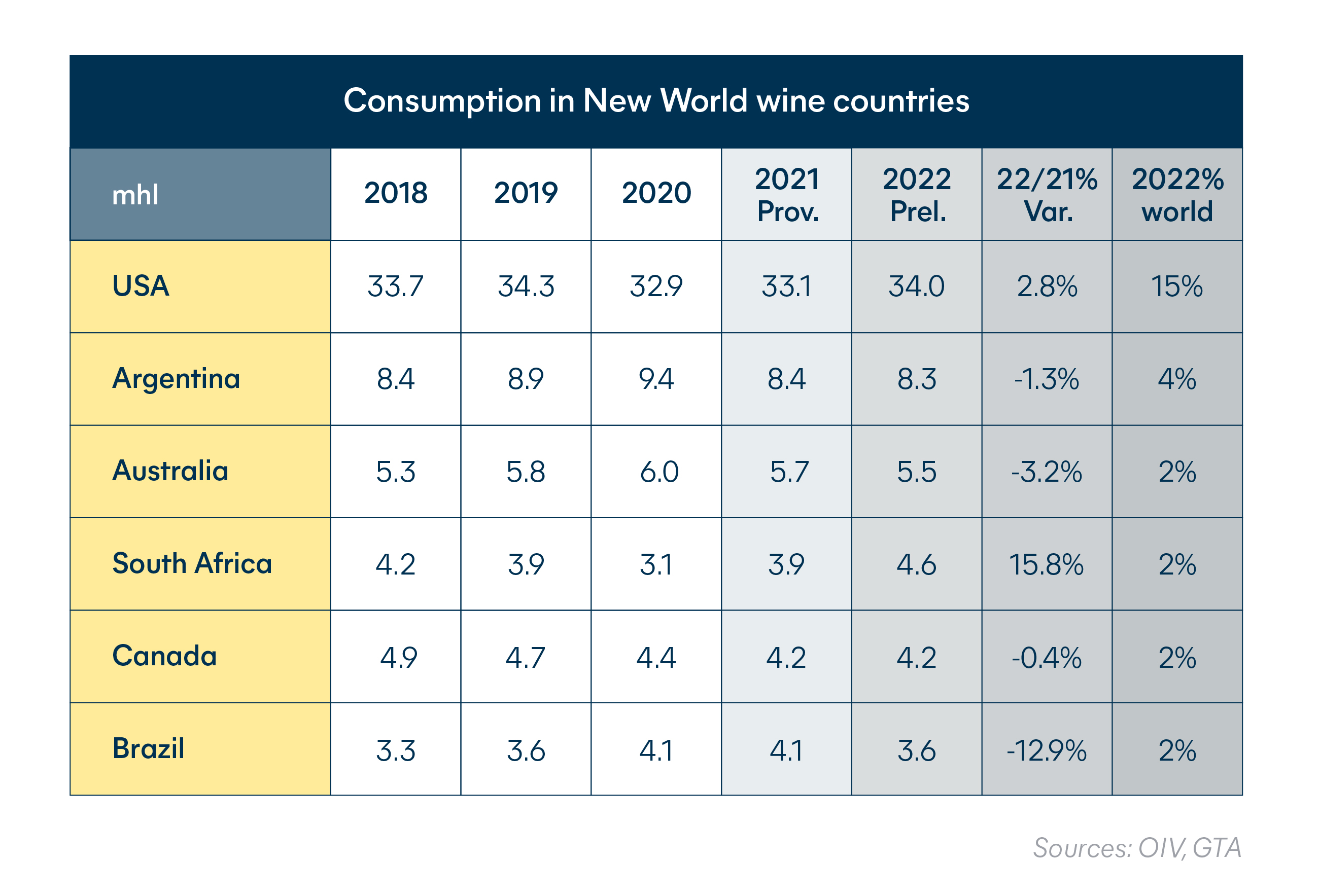

Consumption in New World wine countries

Not surprisingly, the world’s largest wine importer is also the largest consumer. Americans bought 34mhl of wine in 2022. This 2.8% increase on 2021 shows US consumption has recovered to levels recorded before the pandemic.

South Africans are also buying more wine. In fact, the 4.6mhl consumed in 2022 is a 16% increase and the highest level ever recorded in the country.

Consumption is down in Australia for the second year at 3% below 2021 and 2% below its five-year average. South America also saw falls in demand, including in Argentina, its largest market, with 1.3% less wine bought than in 2021. In Brazil, wine consumption reached record highs in 2020 and 2021, but 2022 saw a 12.9% drop to 3.6%. Although this marks a return to pre-pandemic levels.

Other developments of note in 2022

The sparkling wine success story

Globally, sparkling wine is the only category that increased both in terms of volume (+5%) and value (+18%). While it represented only 11% of global export volume, at an average export price of €7.7/l, it came second in value after still bottled wine and contributed 23% to the global total in 2022.

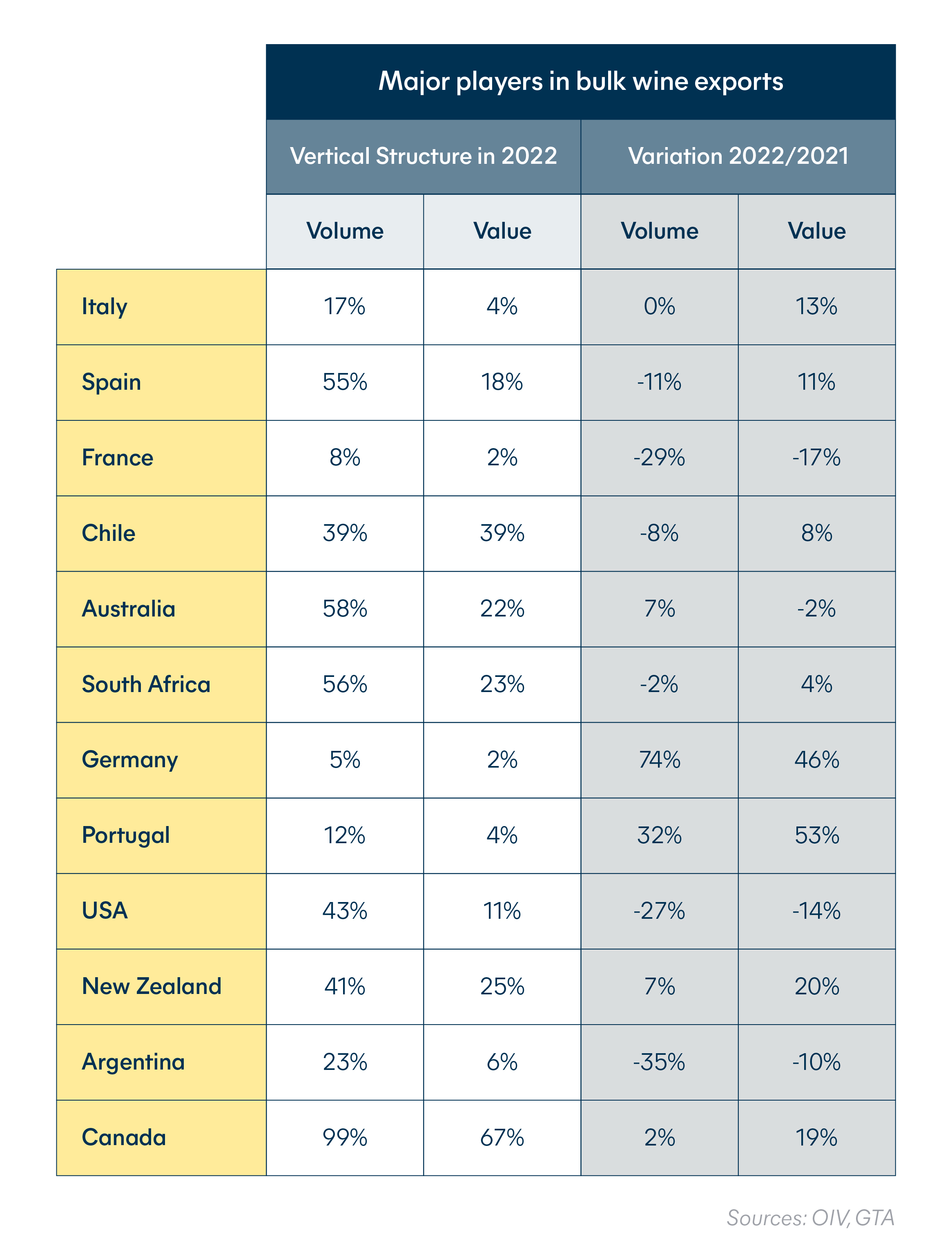

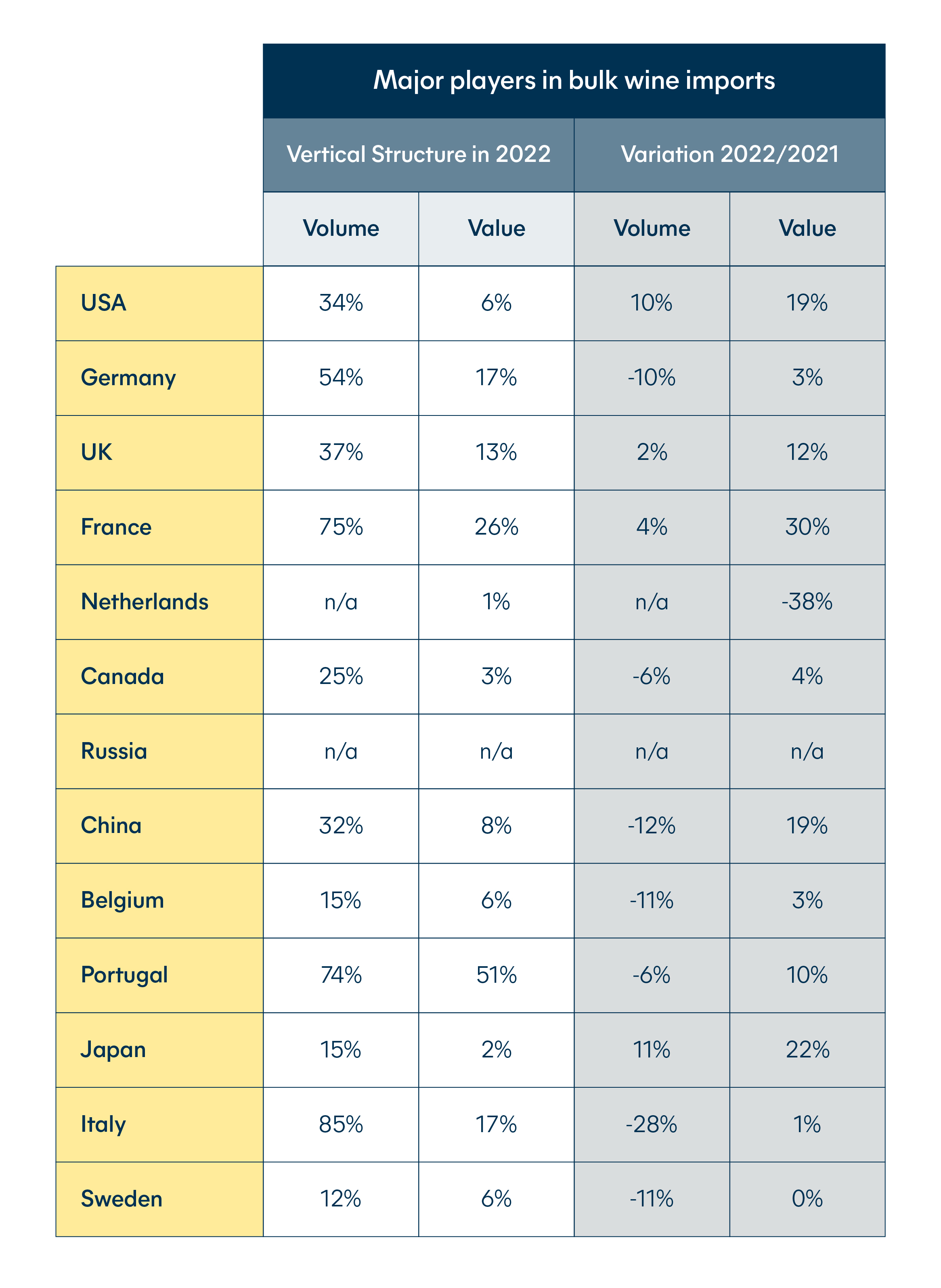

Major players in bulk wine import and export

Overall, bulk wine has a 33% share of total world exports and is the second-largest export category in volume. With an average export price of €78/hl in 2022, it only makes up 7% of the total value of wine exports, but that value is increasing. In 2022, bulk wine export volume was down by 7.2% compared to the previous year but value increased by 5.2% to exceed €2.67bn euros.

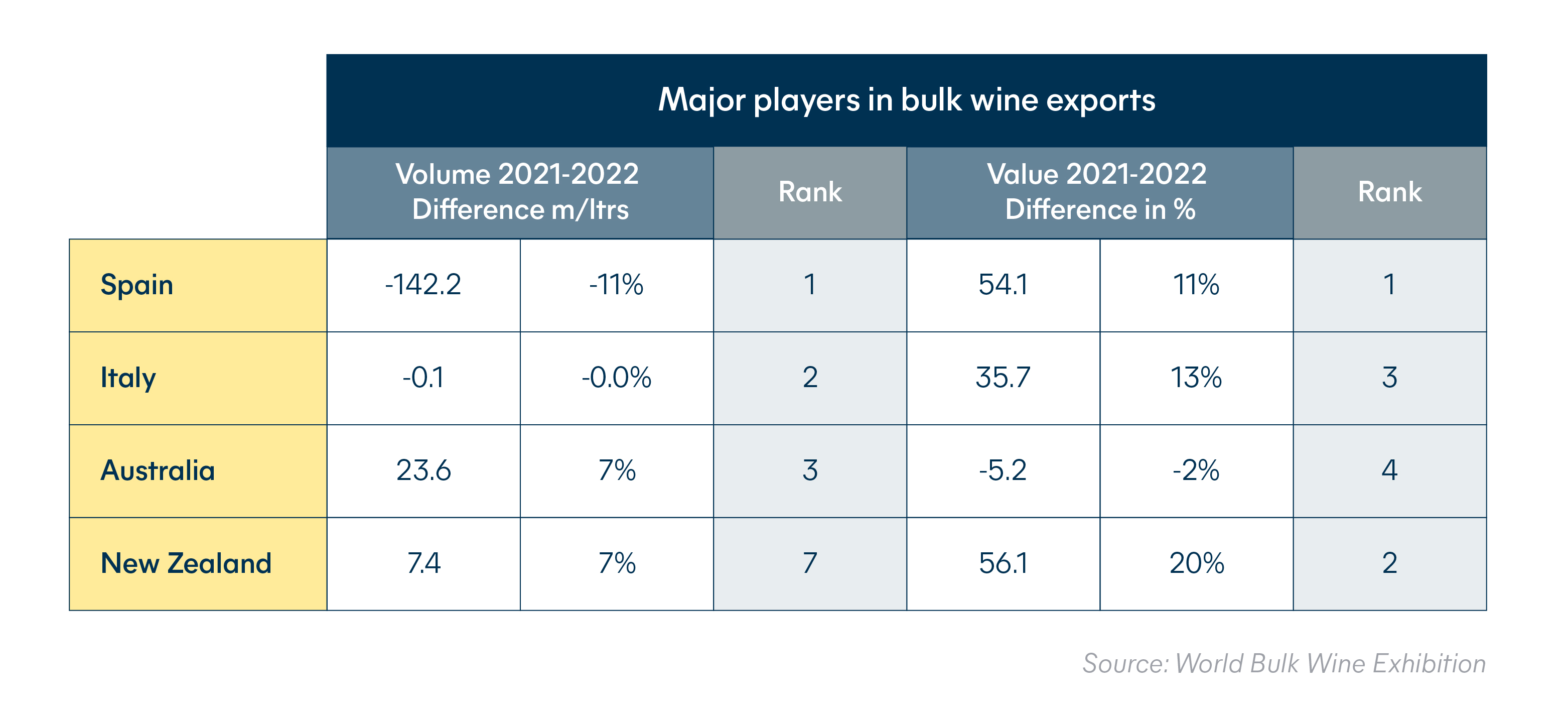

Spain, the number one supplier of bulk wine by value and volume saw an 11% increase in value offset an 11% drop in volume. Its €534m turnover was thanks to a 25% rise in the average price which reached €46/hl.

Italy maintains its position as the second biggest bulk exporter with a volume of 3.74mhl. Value went up by 13% to make €304m putting the country in third position globally.

On the other side of the world, while Australia’s 2.73mhl put it third in volume, the 7% increase couldn’t overcome a 2% drop in value.

In volume, New Zealand comes in seventh but 2022 saw it become the world's second-largest exporting country by value with a 20% increase netting it €340m. This is down to the much higher average price of €282/hl for New Zealand bulk wine exports compared to other big producers.

In terms of bulk wine imports, demand fell by 29% in Italy, although this category still accounts for 85% of Italian wine imports. Bulk made up 75% of French wine imports in 2022. Imports increased by 4% in volume and saw a 30% rise in value. Portugal imported 2.8mhl of wine in 2022, 74% of which was in bulk.

Emerging wine regions in 2022

Poor harvests, economic turbulence, and supply chain problems of recent years have led to higher prices and encouraged buyers to look further afield than usual for their wine imports.

Rather than relying on increasingly expensive traditional sources, importers are exploring more affordable wines from places like Jura, Beaujolais, or Savoy in France and Maremma or Franciacorta in Italy.

Good quality Greek, Portuguese, Hungarian, and Georgian wines are also undergoing a reappraisal thanks to their lower cost.

Let us help you with your wine shipments

Today's wine industry is a dynamic and complex environment, where both consumer tastes and global economic conditions are continually shifting. With the support of a freight forwarder specializing in beverage transport you will be better placed to successfully navigate every situation. Contact Hillebrand Gori, and let our experts help you make the right decisions for your wine imports.

Published 24th July 2023, updated 22nd May 2024

Reviewed by Hillebrand Gori