Tariff, import duty and tax: a quick look

A tariff dictates the rate of duty.

An import (also known as a customs duty) is a fee charged on almost every cross-border shipment of products, and varies based on the Harmonized Tariff Schedule (HTS) codes and their destination. You can look up the item’s HTS tariff code on the HTS database.

Alcohol is based on litres and/or alcoholic strength (proof). While other HTS codes are based on the value of the products, number of pieces or kilo weight.

Alongside common tariff duty, additional excise duty is applicable on alcohol, hydrocarbon oils and tobacco.

Tariffs are usually imposed to regulate the trade of foreign products and depend on country of origin.

Value-added tax (VAT) is a type of consumption tax separate from a customs duty, of special importance in the European Union (EU). It is applied to imported and domestic products and services.

Australia and New Zealand have Goods and Services tax (GST), which is equivalent to VAT.

Who pays for a custom duty and tax, varies according to the Incoterm®.

![]()

Tariffs, duties and taxes: How to calculate the cost of an import duty or tariff on my products?

To calculate how much the duty or tariff on your products are, check your product’s 7-10 digit HTS code and then look for your product on the HTS database here.

Alternatively, ask your freight forwarder who can find this code and do this step for you. Incoterms® are vital to determining whether the seller or buyer takes responsibility for paying the customs duties in any shipment.

We’ve written a useful summary of the current Incoterms® here.

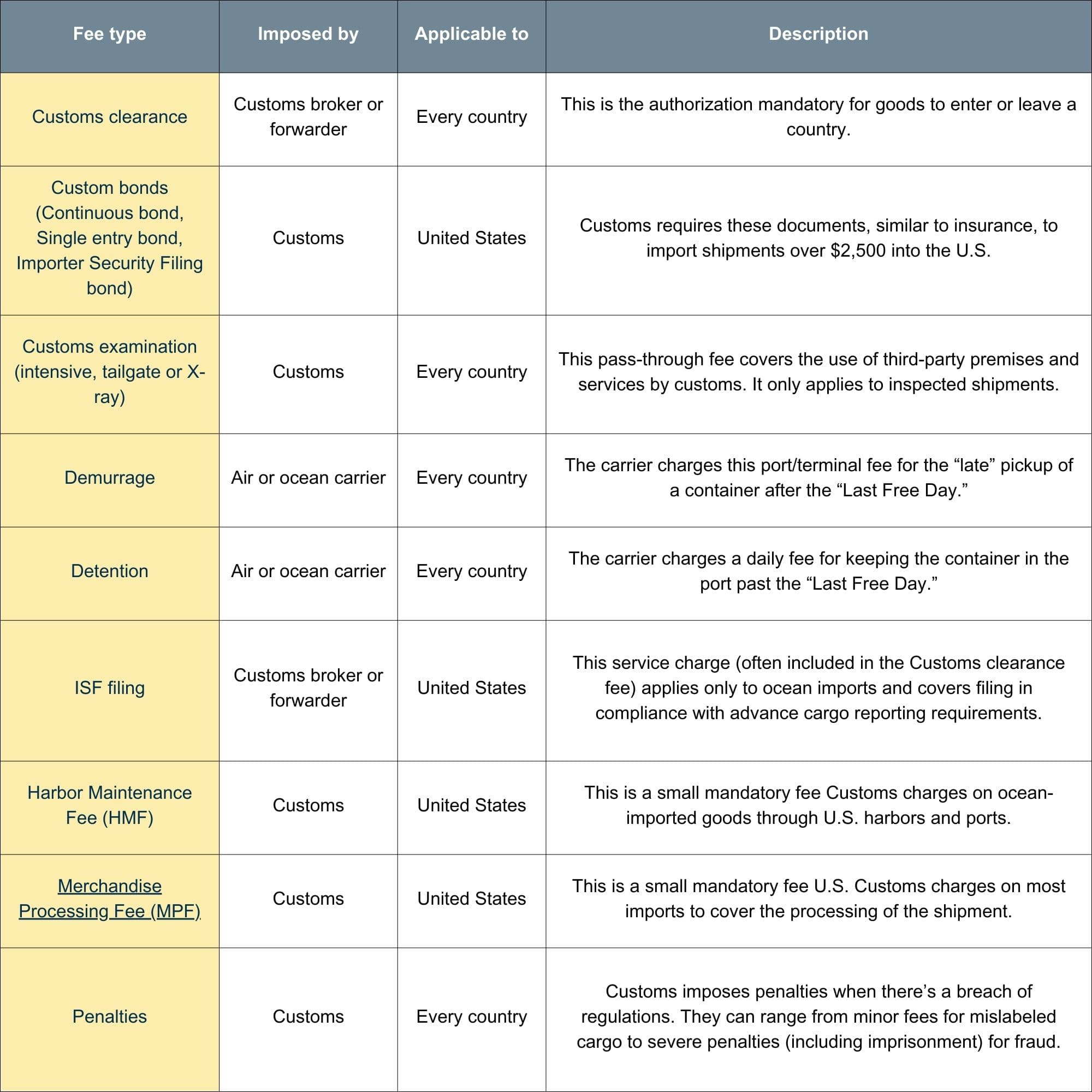

Custom duty charges

Customs duty charges vary depending on the country of origin and product type.

Here is a breakdown of charges explaining who’s liable to pay and why:

Let Hillebrand Gori help you navigate the complex customs landscape

We're experts in global customs regulations and provide custom clearance services worldwide.

Regardless of the origin or destination of your cargo, we'll make sure it gets there safely while adhering to the legal, legislative and regulatory requirements of each country.

If you need a quote or still confused by the terms tariff, import duty or tax is, contact us, we’re here to help!

Published 12th May 2023, updated 27th February 2024