In February 2026, the structure of US tariffs affecting European wine, beer and spirits changed again. Following a Supreme Court ruling, tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were discontinued. A new Section 122 tariff authority now applies to imports entered into the United States.

For European producers and US importers, this is not just a rate adjustment. It is a shift in how duties are calculated and layered. Understanding how Section 122 applies to EU imports is essential for landed cost forecasting, contract allocation and shipment timing.

Article - 22 Jun 2026

Strait of Hormuz: Impact on Fuel Prices, Shipping Costs & Beverage Imports

Read the article

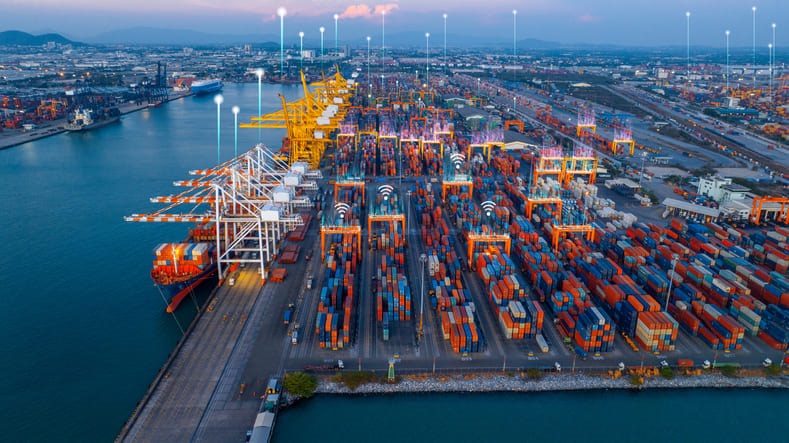

Global transport & logistics