Steady demand, but a slowdown may be on the horizon

Container volumes remained on a strong trajectory into early 2025. Following a record 7.5% growth in 2024, the highest since 2019, demand has continued rising:

- January saw a 5.8% increase year-on-year.

- February followed with a 3% rise, led by strong imports to North America.

- Buoyant trade flows between Asia–Europe and the Middle East have also contributed to sustained volumes.

-ebook-1---global-freight-forwarding/hil---cta-text-1---ebook-global-freight-forwarding-(1).png?sfvrsn=a2292c3e_3)

This growth is largely driven by advance importing, particularly in the US, ahead of potential tariff changes. However, economists now project global GDP to grow by 2.5% in 2025, down from previous forecasts. The moderation in economic outlook could impact future demand levels.

New capacity continues to enter the market

While demand has grown the supply side is evolving rapidly, with new vessel deliveries on the rise:

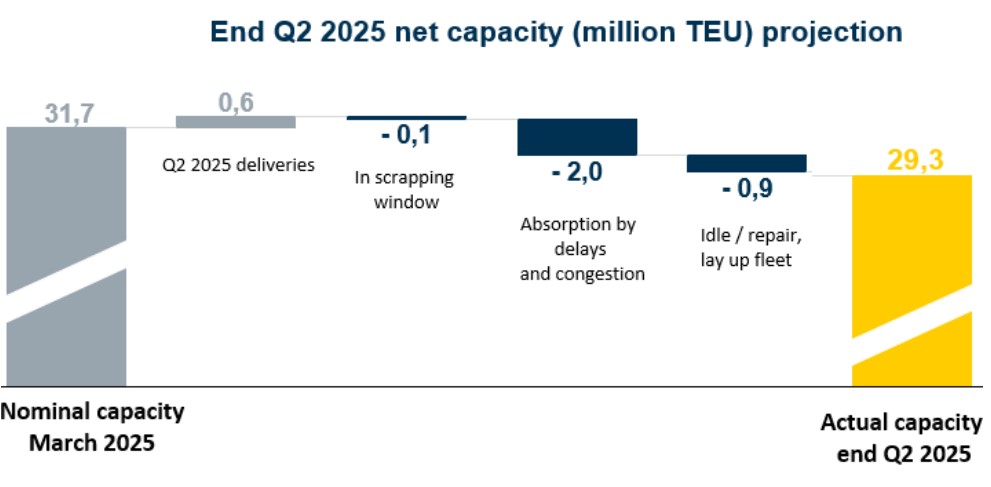

- The global container fleet grew by 10% in 2024, reaching 31 million TEUs.

- An additional 6% increase is expected in 2025, with 1.8 million TEUs set to join the fleet.

- The total vessel order book now stands at a record 9 million TEUs.

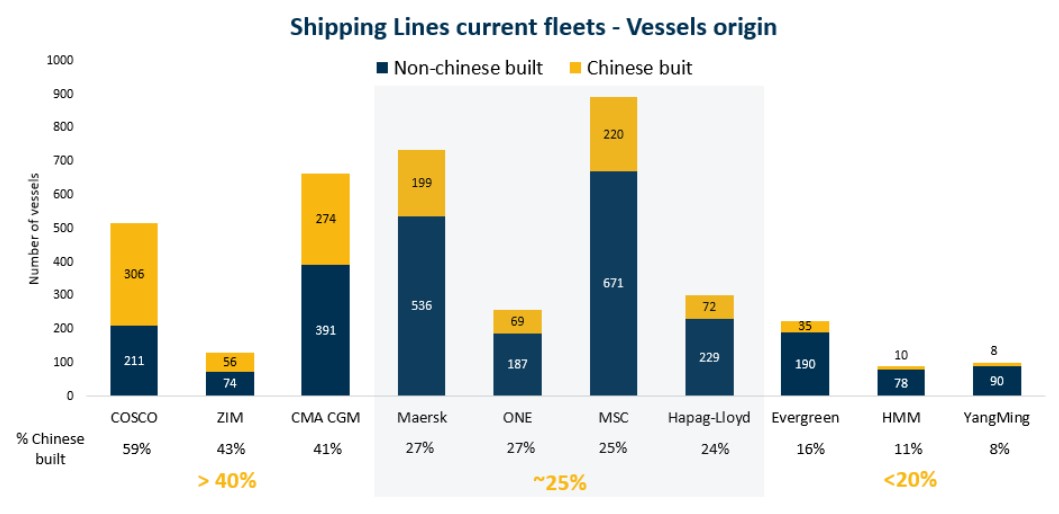

- Over 70% of new vessel orders are held by five key carriers: MSC, CMA CGM, COSCO, Maersk and ONE.

This influx of capacity has not been evenly distributed across all trade lanes. While routes like Transpacific and Asia-Europe have seen increases in vessel deployment, supply to markets such as Latin America, Oceania and the Transatlantic remains comparatively flat, despite ongoing demand.

US Tariff and Chinese vessels policy adds uncertainty to trade flows

Recent analyses highlight the broader implications of tariff uncertainties on transportation sectors. For instance, a MarketWatch article discusses how such uncertainties, coupled with adverse weather conditions, are affecting railroad operations, underscoring the widespread impact on various modes of freight transport.

A temporary 90-day suspension of these reciprocal tariffs, announced on April 9, may prompt a short-term spike in demand, particularly into the US and from Europe. Wine and spirits shipments could see increased movement as importers look to get ahead of any potential changes.

In addition, the USTR position on fees towards Chinese owned and built vessels could bring further disruption.

- A decision expected on April 17 though latest intel suggests this implementation may be postponed altogether

- Proposed tariffs include fees of up to $1.5 million per port call, depending on a carrier’s reliance on Chinese shipbuilding.

- This policy could impact a wide range of carriers and lead to fewer US port calls, potentially increasing ocean freight rates.

We can navigate this together

The freight landscape in April 2025 continues to be shaped by both growth and uncertainty. While container volumes have started strong, tariff policies and ongoing disruptions may alter the balance between supply and demand in the coming months. For importers of wine, beer and spirits, maintaining visibility on market developments will be essential to staying agile and cost-efficient.

Navigating these changing market conditions calls for a logistics partner with expertise and focus. That’s us! With solutions tailored to the specific needs of beverage logistics and a deep understanding of global transport dynamics, We’re here to help make logistics easy. Get in touch today to see how we can support your business.

-ebook-1---global-freight-forwarding/hil---cta-post---yellow.jpg?sfvrsn=5e55bfc5_2)

Reviewed by Hillebrand Gori